Here Is The Real Reason The Fed Restarted QE | Zero Hedge

Posted by M. C. on October 20, 2019

I don’t pretend to understand all this but it appears to me it didn’t help the first couple times.

https://www.zerohedge.com/markets/here-real-reason-fed-restarted-qe

by Tyler Durden

In the past month, a feud has erupted in the financial media and across capital markets between defenders of the Fed, who praise the return of its unprecedented easing in the form of $60BN in monthly T-Bill purchases, by refusing to call it by its real name, and instead the Fed’s fanclub calls it “not QE” (just so it doesn’t appear that ten years after the Fed first launched QE, we are back to square one), and those who happen to be intellectually honest, and call the largest permanent expansion in the Fed’s balance sheet, meant to ease financial conditions and boost liquidity across the financial sector, for what it is: QE.

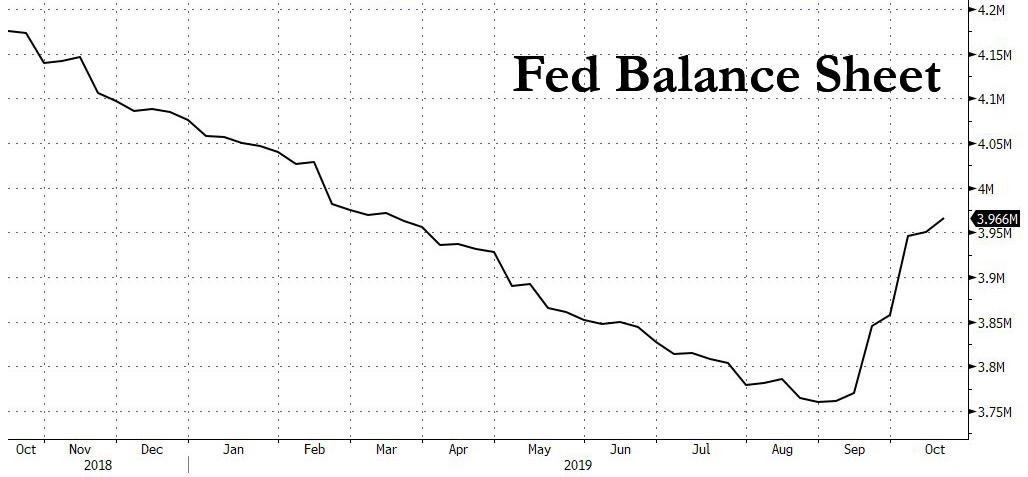

It is this same “not QE” that has boosted the Fed’s balance sheet by $200BN in one month, the fastest rate of increase since the financial crisis.

Yet while the Fed’s desire to purchase Bills instead of coupon Treasuries was dictated by its superficial desire to distinguish the current “Not QE” from previous “True QEs”, even though both tends to inject the same amount of liquidity into the system, which as a reminder is what the Fed’s bailout role in the past 11 years has all been about, and only true Fed sycophants are unable to call a spade a spade, the Fed’s choice raises a rather thorny question of where the Fed will source those T-bills, because as JPMorgan calculates, the net supply of Bills in 4Q19 and 1Q20 is around $115-$130bn while JPM’s economists estimate that at least $200-$250bn of purchases could be required to return reserves to around $1.5tr where they were in early September this year.

That means the Fed might need to source purchases from money-market funds and foreign central banks – which paradoxically would serve to further drain liquidity out of the system. As such, given the limited alternatives, JPM’s Nikolas Panagirtzoglou believes that the Fed may be reluctant to do so and if they do, some may chose to leave cash in the Fed’s ON RRP facility which would represent a drain on reserves and make T-bills a less efficient vehicle for reserve creation.

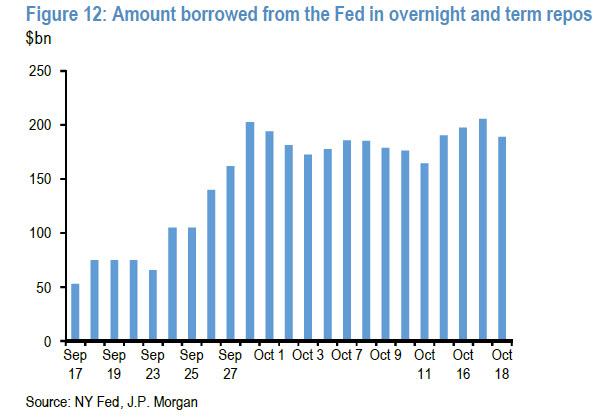

Another key question: what if just returning to the previous reserve baseline is not sufficient, and the Fed needs to return reserves to a higher level than $1.5tr? Indeed, with close to $200bn of reserves injected via overnight and term repos for much of this week…

… helping to return reserves to around $1.5tr on a temporary basis from less than $1.4tr in mid-September, money markets appear especially vulnerable to volatility.

Indeed, in a week when the Treasury’s General Account with the Fed increased by $60bn, depleting reserves, both Fed Funds and the broader OBFR rates median rates rose again to 10bp above IOER on Tuesday Oct 15th after having settled at around 3bp above IOER and at IOER respectively after the quarter-end hurdle had been cleared. And the SOFR median rate rose to 20bp above IOER after having settled at 2-5bp above IOER after the quarter-end effects had settled.

There is another reason why the Fed’s stated intention to only buy Bills will soon have to be adjusted to incorporate short-maturity (at first) Treasury bonds, and it has to do with the total open market purchases planned by the Fed. If the Fed would need to return reserves to a higher level, say to around the $1.7tr level in Dec 2018 when the 75th percentile of the Fed funds market began to persistently print above IOER, this could imply a further $200bn of purchases. JPM finds that “in principle” this could be completed in 2Q20 if the Fed were to sustain T-bill purchases at a pace of $60bn per month, which it set as the initial pace, but it would still imply a longer period of reserves being at a relatively tight level than if $1.5tr would be a sustainable level. But that would assume purchases at a continuous (rather than initial) pace of $60bn/m pace are sustainable, and ignores the prospect that purchases from MMFs and foreign central banks could prompt them leaving cash in the Fed’s ON RRP facility thereby draining some of the intended reserve injection.

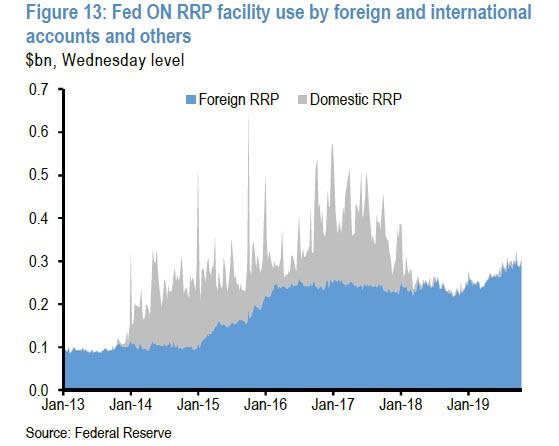

Currently, close to $300bn of cash has been deposited with the Fed via the ON RRP facility, primarily by foreign RRP counterparties for whom the nearly $300bn is close to its recent highs. By contrast, other, largely domestic, counterparties’ use of the ON RRP facility has collapsed to just $2bn, well below a high of nearly $450bn in late 2015, as institutions have a far more pressing needs for cash (liquidity) than collateral securities (“collateral shortage” was the big story in 2014-2017, just ask Zoltan Pozsar).

If T-bill purchases start to put upward pressure on ON RRP facility use, the Fed may eventually need to extend purchases to shorter-maturity Treasury bonds….

Be seeing you

Leave a comment