“With such an agreement, “fractional reserve free banking” proponents say, depositors would know that they are effectively creditors to the bank and that the bank is therefore a debtor to them. This means that the deposits are technically and legally owned by the bank and that what the depositor has is technically and legally a callable loan to the bank. Clear agreements would mean that depositors understand that there is a chance that they won’t be able to get their money (actually, the bank’s money, in this view) immediately in the event of a bank failure. Of course, central banking and government-backed deposit insurance diminish customers’ expectation of bank responsibility…”

https://mises.org/wire/money-your-checking-account-yours-or-banks

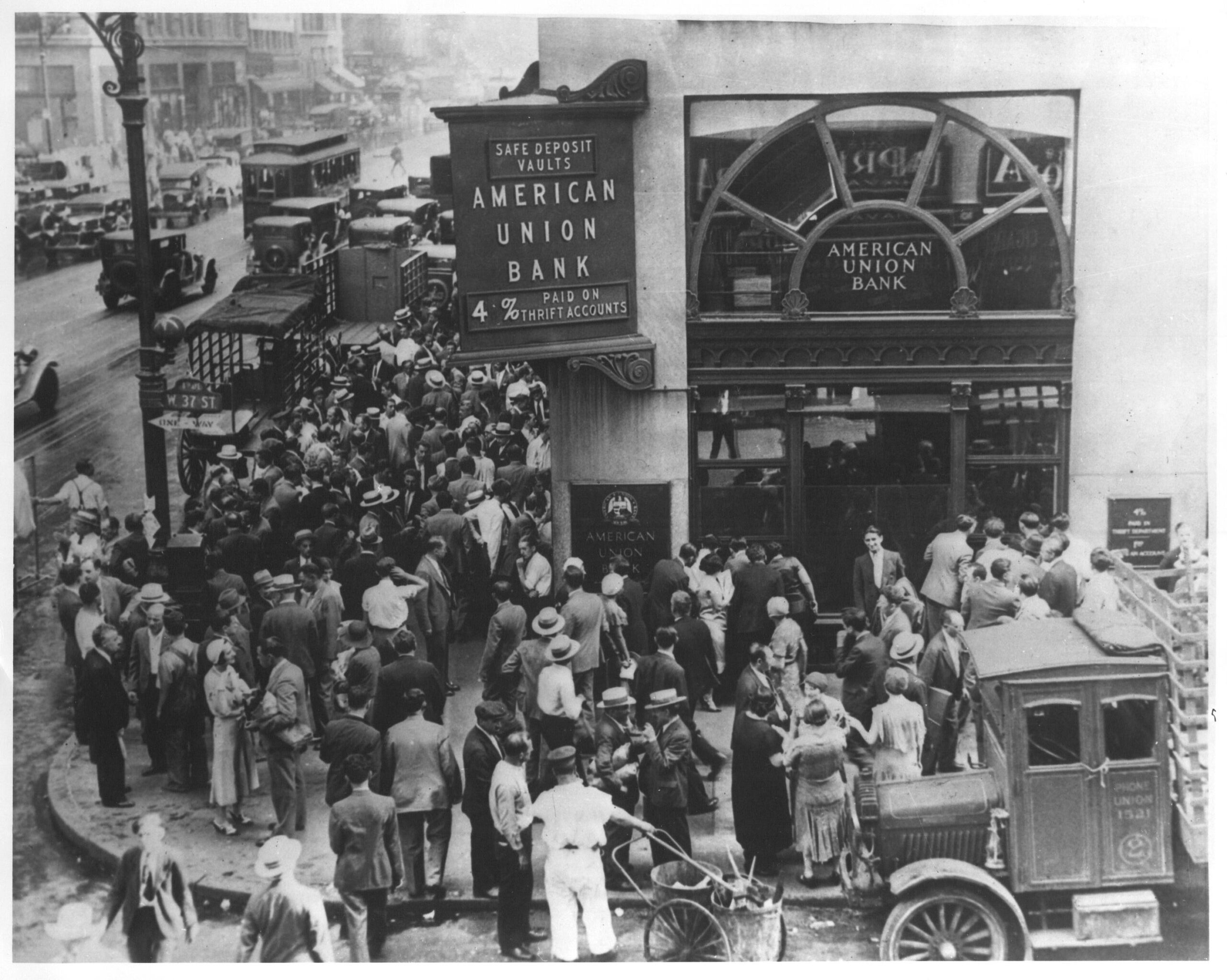

When Silicon Valley Bank and other banks failed earlier this year, the debate over the sustainability of fractional reserve banking resurfaced. Under fractional reserve banking, banks keep only a fraction of customers’ deposits in reserve. The difference is bank credit, such as government debt, mortgages, business loans, and many other kinds of loans. This practice leaves the bank open to a run, in which panicky depositors attempt to withdraw their funds from the bank en masse but the bank doesn’t have the cash on hand. The following FRED graph gives an idea of the extent of the mismatch between deposits and reserves.

But we shouldn’t worry about bank runs because the government is here to help. In the US, the Federal Deposit Insurance Corporation (FDIC) insures checking accounts up to $250,000, and the banking system is regulated by a host of agencies, including the Federal Reserve, which also acts as a lender of last resort. These measures are intended to prevent and mitigate bank runs for the benefit of both the banks and their depositors. Though it should be obvious that they only conceal the fundamental problem and disperse the costs.

Be seeing you