The Bank-Run Phenomenon – The Future of Freedom Foundation

Posted by M. C. on December 3, 2022

Of course, U.S. officials say that an industry-wide banking crisis could never happen in the United States because the U.S. is such a powerful empire. Let’s hope they are right. And let’s just continue acting as though decades of a destructive banking policy, skyrocketing federal spending, spiraling federal debt (now in excess of $31 trillion), and monetary debauchery will come with no adverse consequences.

https://www.fff.org/2022/11/28/the-bank-run-phenomenon/

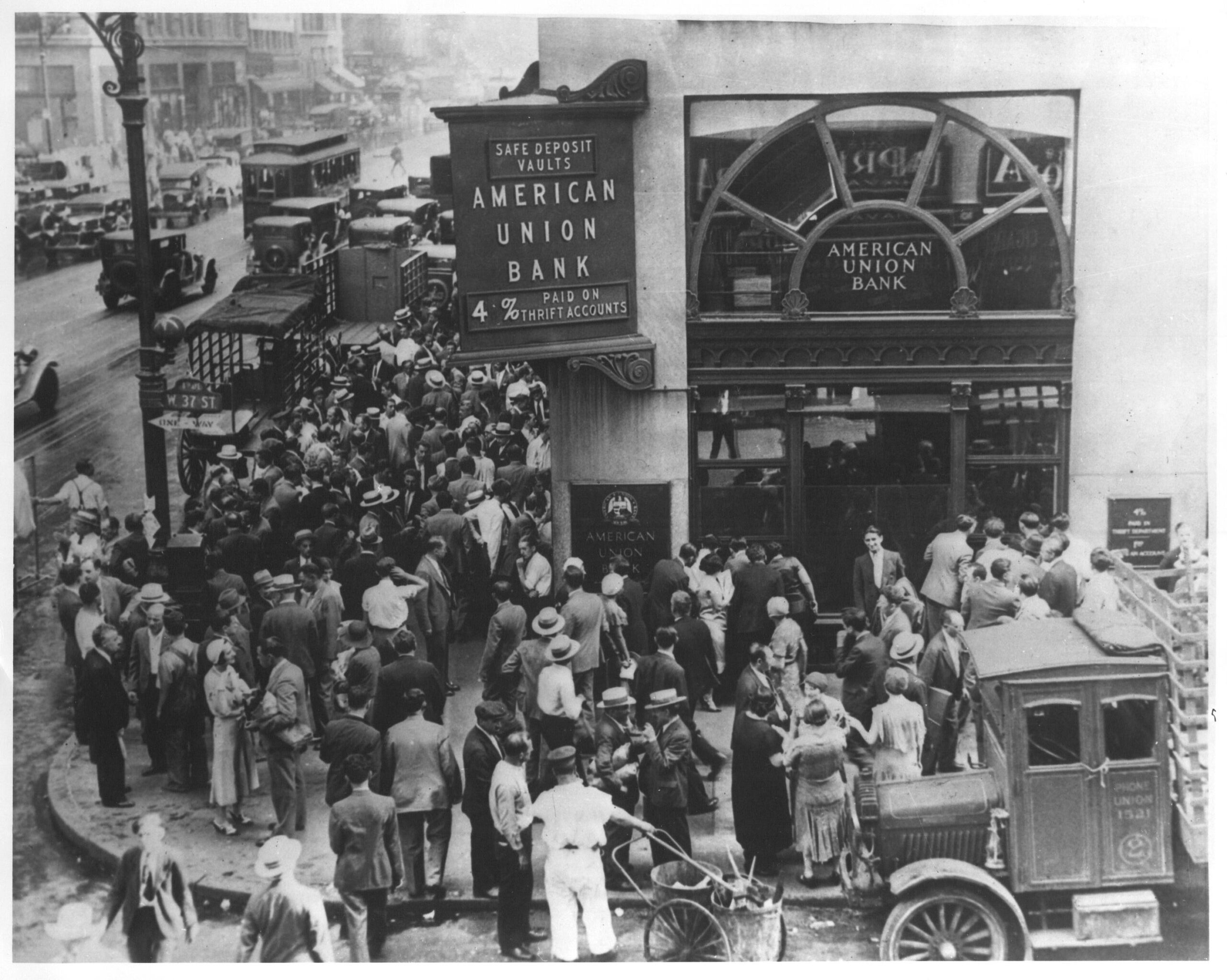

One of the most fascinating phenomena in financial crises is that of bank runs. That’s when panicked depositors rush to their bank to withdraw their money because they’re convinced that the bank is going broke. Everyone tries to withdraw his money before that happens. If the bank does finally go under, the people who failed to withdraw their money are left with a bank that has no money to return to them.

That’s what the FDIC is all about. It insures everyone’s deposits up to a limit of $250,000. The limit used to be $100,000 but U.S. officials, for whatever reason, wanted to make depositors feel even more secure about keeping their money in the bank.

The idea is that people don’t have to worry about losing their money if their bank goes under because the federal government will use taxpayer money to reimburse them. Thus, knowing that their money is “insured” by the government, people have less incentive to rush to the bank to withdraw their money in the event of a potential bank failure.

Of course, one problem with the FDIC insurance is that it enables weaker banks to continue operating, which could make the problem much worse in the future. Without the FDIC, weak banks would go under sooner because people, sensing a problem, would rush to withdraw their money.

Sure, without an FDIC, that would mean that depositors would lose their money. But why should picking the wrong bank be any different from picking the wrong stock or any other investment? We don’t have a Federal Stock Insurance Corporation. If people invest in a stock and the company goes bankrupt, then people lose their money. That encourages people to take care about where they invest their money.

That same degree of care doesn’t exist when it comes to banking. Very few people study the financial condition of the bank in which they deposit their money. That’s because of the FDIC. They know that if the bank goes under, they’re going to get reimbursed by the taxpayers.

But what happens if there is a nationwide banking collapse? The amount of money in the FDIC’s insurance fund is enough to cover losses in several individual banks. But it doesn’t even come close to being able to do that in the event of an industrywide banking collapse.

Be seeing you

Leave a comment