Remember back when the Russia/Ukraine war had just started, and I predicted that Russia and China would launch their own gold backed currency?

At the time, this idea sounded completely foreign, and I was ridiculed for bringing it up. Today, it just become reality. 41+ countries look like they could be returning to a gold standard.

The images plastered all over RT this weekend had headlines like “New Money, New World” and “Gold Standard Will Be Of Great Benefit To Strengthening New Singly Currency”.

“The official announcement is expected to be made during the BRICS summit in August in South Africa,” Kitco reported over the weekend.

“At first glance, a new transaction unit, backed by gold, sounds like good money – and it could be, first and foremost, a major challenge to the US dollar’s hegemony,” Thorsten Polleit, chief economist at Degussa, said.

In other words, Roosevelt and the Congress changed the Constitution without ever getting the Constitution amended. What they did was classic dictatorial conduct, the type of conduct one finds in totalitarian regimes.

The United States once had the finest monetary system in history. It was a system that the U.S. Constitution established. It was a system in which the official money of the United States consisted of gold coins and silver coins.

We often hear that the “gold standard” was a system in which paper money was “backed by gold.” Nothing could be further from the truth. There was no paper money in the United States. That’s because the Constitution did not empower the federal government to issue paper money. It also expressly prohibited the states from issuing paper money.

The Constitution used the term “bills of credit.” That was the term people at that time used for paper money. The Constitution expressly forbade the states from issuing “bills of credit” or paper money. It also did not delegate the power to issue “bills of credit” or paper money to the federal government.

Instead, the Constitution empowered the federal government to “coin” money. At the risk of belaboring the obvious, one does not “coin” money out of paper. One “coins” money out of such metallic commodities as gold and silver.

The Constitution also expressly forbade the states from making anything but gold and silver coins “legal tender,” or official money, which further established the intent of the Framers.

The Constitution also empowered the federal government to borrow money. That’s what U.S. debt instruments — bills, notes, and bonds — are all about. But even though these debt instruments oftentimes circulated as “semi-money” in economic transactions, everyone understood that they were not money itself. Instead, they were promises to pay money, which meant promises to pay gold coins and silver coins.

Soon after the enactment of the Constitution, the U.S. government began minting gold coins and silver coins. Gold coins and silver coins remained the official money of the American people for more than a century. Those coins ranked among the most honest coins in history.

The gold-coin-silver-coin standard — and the monetary stability that came with it — was a major contributing factor to the enormous rise in the standard of living of the American people in the 19th century and early 20th centuries, especially in the period from around 1880 to 1915.

Of particular importance was that the American people did not have to worry about inflation reducing the value of their assets, investments, and income. That’s because the federal government lacked the means to inflate the quantity of gold coins and silver coins in the economy.

All that changed in the 1930s. Using the Great Depression as an excuse, President Roosevelt and his Congress abandoned the monetary system established by the Constitution and that had been in place for more than a century. In its place, they installed a paper-money standard. Possession of gold coins was deemed to be a felony. Anyone who was caught possessing what had been the official money of the nation for more than a century, faced a criminal prosecution, a 10-year jail sentence, a $10,000 fine, and forfeiture of his gold to the government.

The good news is that Washington’s plans for world domination are bound to fail as China and Russia have a revived alliance, which also appeals to and is open to other powers. The bad news is that this will lead to the drawn-out collapse of the dollar, which Washington will attempt to parlay into a new central bank digital currency to accompany an increased crackdown on opposition within the dwindling empire.

In 1971 Richard Nixon took the US off the last feeble vestiges of the gold standard, otherwise known as the Bretton Woods Agreement. That system had been a bizarre gold-dollar hybrid where the dollar was the world reserve currency but the US agreed to keep the dollar backed by gold. Henry Hazlitt’s bookFrom Bretton Woods to World Inflation explains the consequences of this situation well.

The end of this system left a vacuum at the heart of world financial affairs, one that needed to be filled quickly. The dollar, now unmoored by gold, remained the default currency for international trade, but without the confidence derived from its former gold backing, the US needed to bolster its credibility lest other more enticing options appeared to displace the dollar’s hegemony.

During the 1973 Arab-Israeli war, Organization of the Petroleum Exporting Countries (OPEC) had gained leverage by imposing an oil embargo, which caused serious disruptions in the global economy. In 1974 Henry Kissinger brokered a deal: Israel would back off its territorial ambitions, the Arab states would end the embargo, and oil would be traded in dollars. Thus, the petrodollar was born.

Every economy needs energy, and Saudi Arabia supplies plenty of oil, meaning that the dollar was backed up by a valuable commodity that would always be the recipient of demand. Everyone wants oil, and the Saudis would only trade it for dollars, so the dollar became unavoidable in international trade, reaffirming its status as the world reserve currency.

Even if others would have preferred a neutral, market-based currency not subject to manipulation, the opportunity cost of foregoing oil was far higher than the cost of having to use the dollar. A global medium of exchange selected by the market would have been more economically efficient, but given that the US and the Saudis possessed the ability to impose a politically motivated system, nobody was willing to bear the costs to create an alternative as long as the dollar was managed fairly sensibly.

Washington and the Gulf States benefit enormously from this situation. The petrodollar gives the Fed extreme license to print currency and export its inflation. If other countries are forced to use your currency, that gives you a lot more room to debase it. Imports are made cheaper with the high purchasing power of the dollar, and exports are propped up because the easiest way to spend dollars is to buy American products.

All this amounts to Washington essentially taxing world trade. The Gulf States benefit in the same ways by having enhanced access to the world reserve currency. Their oil is given priority in world markets compared to competitors opposed by Washington, such as Iran. They are also just simply given financial aid by Washington for participating in this scheme.

However, there are consequences for the countries involved. Even if the US has largely avoided extreme domestic consumer price inflation by circulating dollars around the world, the business cycle consequences of inflation are unavoidable. For example, the 2008 recession was severe yet unaccompanied by extreme inflation before or after. Holding the world reserve currency has also given the US a free ride with far less need to produce valuable goods and services. The dollar holds its value because there has always been global demand for it, so it has been possible to print money to prop up the US economy by consumer spending without an extreme loss of value in the dollar. But there is now very little worth in the underlying US economy.

One school of thought has it that, although the US has long claimed that it possesses roughly 8,000 tonnes of gold in Fort Knox, there has not been an audit of Fort Knox since 1953. (That’s not encouraging.) Is it 8,000 tonnes? 4,000? None? We’re unlikely to ever get a truthful answer on this question.

In 1971, the US abruptly went off the gold standard, and in making the public announcement, US President Richard Nixon looked into the television camera and said, “We’re all Keynesians now.”

I was a young man at the time and had previously bought gold, albeit on a very small scale, but I recall looking into the face of this delusional man and thinking, “This is not good.”

However, the world at large apparently agreed with Mister Nixon, and within a few years, the other countries also went off the gold standard, which meant that, from that point on, no currency was backed by anything other than a promise.

Party Time

It didn’t take long before countries began playing with their currencies. At one time, the German mark, the French franc, the Italian lire, and the British shilling had all been roughly equivalent in value, and four or five of any one of them was worth about a dollar.

That had already begun to change prior to 1971, but following the decoupling from gold, the governments of the world really began to see the advantages of manipulating their own currencies against the currencies of other nations.

From that point on, a currency note from any country, which was already no more than an “I owe you,” was increasingly degraded to an “I owe you an undetermined and fluctuating amount.”

This fixation with monetary manipulation began much like the 1960s youths’ experimentation with drugs, and by the millennium, had morphed into something more akin to heroin addiction. Unfortunately, those who had become the addicts were the national leaders in finance and politics.

Well, here we are, in the second decade of the millennium. The party has deteriorated and is soon to come to a bad end.

As we get closer, those of us who have, for many years, predicted an eventual realisation that Mister Keynes and Mister Nixon were dead wrong and that the world will once again look to gold are, at this late date, gaining a bit of traction.

We’re seeing an increase in the number of people who recognise that all fiat currencies eventually come to an end and gold will continue to shine.

But there are two remaining questions that have even the best of prognosticators puzzling.

1. What Will the Role of Gold Be in the Future?

When currencies collapse, will there be an immediate and complete switch to gold? Unlikely.

Will further fiat currencies be put forward as solutions to paper money? Almost definitely.

Will future currencies be backed by gold? Probably, especially as so many governments and banking institutions are quietly scrambling to buy gold whilst trying not to let on the extent of their stockpiling.

Will gold-backed currencies stabilise money for the rest of our lives? Quite unlikely.

Even those countries who may agree to audits to demonstrate they own the gold they claim to own will, at some point in the future, look for ways to “do a Nixon” and once again get off the gold standard. (The short-term benefits of fiddling with currency is too tempting.)

2. Who’s Got the Gold?

Currencies come and go in the world with remarkable frequency (the last hundred years has been witness to over twenty hyperinflations worldwide).

In that quiet scrambling we were talking about, no one is being really truthful about how much gold they have. In addition, even between the foremost experts on the subject (and here, I refer not to the pundits on television, but to those economists that I personally hold in the highest regard), there is broad speculation as to who holds what.

One school of thought has it that, although the US has long claimed that it possesses roughly 8,000 tonnes of gold in Fort Knox, there has not been an audit of Fort Knox since 1953. (That’s not encouraging.) Is it 8,000 tonnes? 4,000? None? We’re unlikely to ever get a truthful answer on this question.

In addition, the US has held roughly 6,000 tonnes of gold for European countries since the Cold War.

Now that the US has become the world’s foremost debtor nation, Europe is getting a bit antsy, and some are asking to have it back. In response, the Federal Reserve has sent Germany a small portion of their gold but avoids shipping the remainder and denies them even the ability to inspect the remainder. (Again, not encouraging.)

On the other hand, we have equally astute economists—US government insiders—who state that they are fairly certain the gold is there—in both Fort Knox and the New York Federal Reserve Bank’s underground vault. In the latter case, they state that, although much or all of the gold has been leased to the bullion banks, it has never left the building.

What does this mean to the rightful owners? There are multiple legitimate claims on the very same bars of gold.

As a result, credit is centralized in the system of credit-expanding banks and investment decisions are dictated by the short-term logic of said system. Changing diets is just one consequence of the distortions engendered, albeit one that no one, pace Selgin, has investigated until now.

In my article on the gold standard published in the Journal of Libertarian Studies back in May, I suggested that the destruction of the gold standard led to changing consumption patterns, specifically to a drop in the consumption of beef. The eminent economist George Selgin was kind enough to suggest that this was a novel argument, although in truth, in that essay I did no more than hint en passant at a possible connection between fiat money and changing consumption patterns, without explaining what the causal factors at work are. Therefore, I think the thesis bears restating and expanding upon.

Changing Food Consumption Patterns in the Twentieth Century

The change in meat consumption was a global phenomenon, but for present purposes, I will focus on the American case, although the same causal factors are at work, and probably to a greater extent, in the rest of the world. The US Department of Agriculture’s Economic Research Service (ERS) compiles and publishes copious data on food availability, that is, how much of various foods are available to the American consumer. Various kinds of meat are partial substitutes for each other, as are, of course, other foodstuffs; however, it seems a fair assumption to say that, in general, people would consider beef, pork, and poultry (the top three meats) the closest substitutes. Only in extreme cases would one consider, say, soy a substitute for tasty beef.

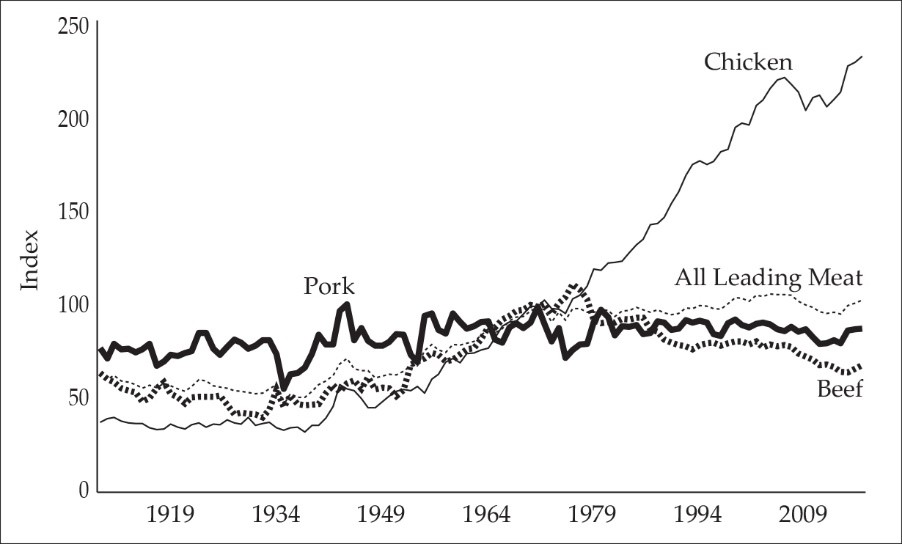

The ERS dataset for meats covers the period 1909–2019 and measures availability in pounds per capita. In 1909, there were 51.1 pounds of beef, 41.2 pounds of pork, and 10.4 pounds of chicken available per capita, for a total of 102.7 pounds of all meats per capita. In 2019 the figures were, respectively, 55.4, 48.8, and 67.0 per capita, for a total of 171.2 pounds of all meats per capita. While meat consumption had gone up, the composition of the diet had changed drastically. If we add the fact that veal and delicious lamb, minor components in 1909 at 5 and 4.4 pounds per capita, respectively, had virtually disappeared from the diet in 2019, the change becomes even more noticeable.

The following graph indexes the changing composition of meat availability over the century (1971=100). As we see, there is a steady and drastic rise in chicken availability from about the early 1950s, while the expansion of beef availability peaks in 1976 and then drops steadily back toward the 1909 level. While availability of all meats expands until about 1970, it stagnates thereafter.

If we look at changes in the relative prices of the various foodstuffs over the long run, a similar picture emerges. Beef prices have increased since the middle of the twentieth century, while other prices have fallen.

Unfortunately, poultry prices are not listed in the dataset. However, we can approximate them by looking at grain prices, as this is a main input in the raising of chicken.

I have here chosen barley and corn prices, but it does not matter much, since the trend is similar for the prices of all grains. Prices have decreased since midcentury despite some fluctuations in the seventies and are now far below the level that prevailed for decades. Beef prices, on the contrary, have trended much higher and were in 2020 about double the level in 1900 or 1850. If we consider the relative price of beef, it is much, much higher, so we should not be surprised that meat consumption has shifted to cheaper substitutes: pork and especially chicken. It is clear that a fundamental change has happened in modern food production.

Kristoffer Mousten Hansen is a research assistant at the Institute for Economic Policy at Leipzig University and a PhD candidate at the University of Angers. He is also a Mises Institute research fellow.

With the possible exception of international trade, no topic in economics contains more myths than monetary theory. In the present article I address four popular opinions concerning money that suffer from either ambiguity or outright falsehood.

One: “Money represents a claim on goods and services.”

Although there is a grain of truth in this view, it is quite simplistic and misconceives what money really is.1 Money is not a claim on goods and services, the way a bond is a legal claim to (future) cash payments or the way a stock share is a claim on the net assets of a company. On the contrary, money is a good unto itself. If you own a $20 bill, no one is under any contractual obligation to give you anything for it.2

Now of course, in all likelihood people will be willing to exchange all sorts of things for your $20 bill; that’s why you yourself performed labor (or sold something else) to obtain it in the first place. Nonetheless, if we wish to truly understand money, we must distinguish between credit liabilities on the one hand, and a universally accepted medium of exchange (i.e., money) on the other.

Two: “The purchasing power of money equals the supply of real output divided by the supply of money.”

As with the first view, this one too has a grain of truth. Specifically, if everything else is held equal, then the “price level” (if we ignore the problems with measurement and arbitrariness) will go up if the money supply grows by more than real output, and will go down if real output grows by more than the stock of money.

However, other things need not be equal, in particular the demand to hold money. As with every other good, the “price” of money (i.e., its purchasing power—or how many units of radios, televisions, etc. people offer in order to receive units of money) is determined by the supply of dollars and the community’s demand to hold dollars. A given stock of money can be consistent with any price level you want, so long as you are allowed to change the demand for money.

For example, even if output and the stock of money stayed constant, all prices could double if everyone in the community wanted to cut in half the purchasing power of his or her cash balance. How is this possible? Initially everyone thinks he or she is holding “too much” cash and so tries to spend it. But since the merchants too think they are holding too much, they agree to sell only at higher prices. (If this seems odd to you, consider: Even if you are uncomfortable with $1000 in your wallet—maybe you just won big at the casino—if someone walked up and offers you another $1000 for your shoes, you’d probably accept.)

If we ignore all of the real world complications caused by timing issues, it’s easy to see that in the new equilibrium, where everyone is content with his or her cash holdings, nothing “real” will have changed. Instead, the unit price of everything (in terms of dollars) will have doubled, so that even though the per capita quantity of dollar bills is still the same, now the average person can only buy half as much real stuff with the money in his wallet. Of course this type of example (which I picked up from Milton Friedman) is very unrealistic, but it does serve to illustrate the point that prices are not a mechanical function of physical stocks of goods and dollar bills. On the contrary, people’s subjective valuations are also critical.

Three: “Under a gold standard the money is backed by something real, whereas under our present system dollar bills are backed up by faith in the government.”

Again, I sympathize with this type of view, but when my upper-level students write such things on their exams, I have to take off points for imprecision. Strictly speaking, under a gold standard the money isn’t backed by anything; the money is the gold. Now if we have a government that issues pieces of paper that are 100% redeemable claims on gold, I wouldn’t classify those derivative assets (i.e. the pieces of paper) as money, but perhaps as money certificates. Yet this is a minor quibble.

My real objection to the view quoted above is that it denies that our current fiat currency is really money. Although (as a libertarian, Austrian economist) I fully condemn the monetary history of the United States, and deplore the means by which the public was forcibly weaned from the gold standard, nonetheless it is simply misleading and inaccurate to deny that the green pieces of paper in our wallets and purses are genuine money. They satisfy the textbook definition: They are a medium of exchange accepted almost universally in a given region. No one is forcing you to accept green pieces of paper when you sell things. (If you don’t want anyone foisting pictures of US presidents on you, then just charge a billion US dollars for everything you sell.) The fact that government coercion (past and present) is necessary to maintain this condition is irrelevant; cigarettes really circulated as money in World War II P.O.W. camps, even though this wouldn’t have occurred without the artificial and coercive environment in which those traders found themselves.

Four: “Deflation is undesirable because it cripples investment. If prices in general are falling, no one will invest in real goods because he can earn a higher return holding cash.”

Although this last myth is understandable when espoused by the layperson, it is inexplicable that some trained economists believe it. (For three examples: An NYU professor used it to “shoot down” my Misesian friend in class, Wikipedia’s entry on deflation mentions this argument, and even Gottfried Haberler advances a version of it in this essay.) For one thing, the argument overlooks the fact that there were many years of actual deflation in industrial economies on gold or silver standards; I don’t think investment fell to zero in every single such year. So clearly something must be wrong with the argument.

Specifically the argument fails because it carelessly assumes that the relevant data for an investor are the spot prices of a particular good from one year to the next. But this is wrong. For example, suppose someone is considering investing in bottles of fermenting grapes that will be ready for sale as wine in exactly one year.3 The rate of return on this investment concerns the 2005 price of the grapes and the 2006 price of wine. So let us further refine the example and suppose that all prices fall 50% every year; i.e., there is massive deflation and presumably no one should be willing to invest in wine or anything else.

Yet there is no reason to jump to this conclusion. For example, the 2005 price of the bottle of fermenting grapes might be $100 and the 2005 price of a wine bottle might be $400, while the 2006 price of the bottle of grapes will be $50 and the 2006 price of a wine bottle will be $200. (Notice that, as stipulated, all prices have fallen by 50% per year.) Would our investor prefer to hold his cash, which in a sense appreciates at a real rate of 100% per year? Not at all! With our numbers, the investor would earn a 100% nominal (not just real) return on his money if he invests in the wine industry: He pays $100 for a bottle of fermenting grapes in 2005, then waits one year and sells the resulting bottle of wine for $200.

Had our investor sat on his $100 in cash in 2005, its purchasing power would have risen from 1/4 of a bottle of wine (in 2005) to 1/2 of a bottle of wine (in 2006). But by investing the cash, his purchasing power goes from 1/4 of a bottle in 2005 to 1 bottle in 2006. Once we allow for the prices of capital goods and raw materials to adjust to expectations of deflation, there is no reason for falling prices to hamper investment whatsoever. 4

Conclusion

Most of the myths concerning money are easily exposed when we consider what money is. Some of the more subtle myths, especially those concerning price deflation, are exposed once we consider the intertemporal price structure. On both counts, the Austrian School of economics serves us well.

[Originally published February 28, 2006, as “What Money Isn’t”]

1. For a more systematic introduction to the Austrian theory of money, see this article.

2. Even legal tender laws don’t affect this statement. If you owe someone, say, $1,000 and the government says a particular $20 bill counts as partial payment, that’s not the same as saying that someone owes you an item in exchange for the $20 bill. Rather, it’s just the government declaring that your debt can be partially satisfied with the $20 bill in question. (Naturally I oppose legal tender laws.)

3. I suspect that this story is far from an accurate description of wine making, but it was the easiest way for me to illustrate my point.

4. A sophisticated critic could answer that the true problem with deflation is not that it would completely eliminate all investment, but rather that investment would stop at the point at which the marginal real return equaled the real return from holding cash. I’m not sure that even this version of the argument is valid, but in any event it’s not what many of the economists (such as the Wikipedia author) seem to be saying.”

In 1260, Kublai Khan created the first unified fiat currency. The jiaochao was made from the inner layer of bark of the mulberry tree. It’s of interest that the mulberry tree was quite common in Mongolia. What allowed Kublai Khan to get away with treating tree bark as currency was that each bill was cut to size and signed by a variety of officials. They affixed their seals to each bill. To further ensure authenticity, forgery of the chao was made punishable by death.

But even then, why would people accept bark as being of the same value as gold and silver, which had successfully served as “money” for thousands of years? Well, to begin with, the chao was redeemable in silver or gold. But just to make sure it was accepted, Kublai decreed that refusing to accept it as payment was also punishable by death.

Today, we’re more sophisticated. Governments no longer threaten to kill people for refusing to use a fiat currency; they just make it extremely difficult to deal in anything but fiat currency.

At the time, Kublai was involved in an ongoing war with the Song. The war had drained the treasury and Kublai was finding it difficult to continue to finance the war. And so, in 1273, he issued a new series of the currency without having increased the gold and silver in the treasury.

In 1287, Kublai’s minister, Sangha, created a second fiat currency, the Zhiyuan chao, to bail out the previous one, to deal with the budget shortfall. It was non-convertible and was denominated in copper cash.

There’s an old saying that, if you find yourself in a hole, the first thing to do is stop digging. Yet, throughout history, leaders, having created a Ponzi scheme of fiat currency and finding out that it has its pitfalls, invariably keep digging ever faster. Read the rest of this entry »

The longer a fiat currency is the coin of the land, the more one is led to believe that nothing should be in short supply, since everything is bought with money and money need not be in short supply.

What causes the seemingly unfounded confidence in socialism we encounter more and more in the news media and among political activists? In the Extinction Rebellion movement, for example, activists are quite certain they have learned that there is an alternative to markets as the means to economic prosperity. It’s a means that does not involve meeting the legitimate needs of one’s fellow men in the marketplace.

It is likely not a coincidence that most people living today have lived most of their lives in a world dominated by fiat money. It has now been nearly fifty years since the United States broke all ties between the dollar and gold. It’s been even longer since other major currencies were tied to gold at all. Consequently we now live in a world where the creation of wealth is seen by many as requiring little more than the creation of more money.

In this kind of world, why not have socialism? If we run out of money, we can always print more.

Unlimited Money Feeds the Myth of Unlimited Real Resources

The world was on a watered down version of a gold standard until 1971 when the US abandoned its solemn promise — the 1944 Bretton Woods Agreement — to back the dollar with gold at $35 per ounce. Gold backing of a currency provided a solid intellectual foundation of reality that few even recognized existed within themselves; (i.e., that we live in a world of scarcity and uncertainty). This reinforced the idea that wealth has to be built. It cannot be conjured out of thin air, just as gold cannot be conjured out of thin air.

But fiat currency can be conjured out of thin air and in enormous amounts. The longer a fiat currency is the coin of the land, the more one is led to believe that nothing should be in short supply, since everything is bought with money and money need not be in short supply. Those who know only unlimited fiat money soon demand free healthcare and free higher education as a right. And why not? Unlimited money will pay for it. Into this never-never land comes demands for scrapping the fossil fuel underpinnings of our modern economy by those who understand nothing of how an economy works. But, apparently one does not need to understand technical limitations, because there are no technical limitations. The “barbarous relic” (gold) had once limited the money supply and thusly seemed to limit the supply of vendible goods. Gold has been replaced by unlimited fiat money. Now it seems that unlimited aggregate demand can be funded by unlimited fiat money, leading to a world of plenty. Designer of the Bretton Woods Agreement Lord Keynes says so in this very insightful short video.

Fiat Money Turns the World Upside Down

The psychological impact of a lifetime within a fiat money economy cannot be underestimated. One’s world is turned upside down. For many, financial success becomes prima facie evidence of exploitation of the masses rather than something to be admired and to which one could aspire also. With more wealth seemingly available at the click of a computer button, only an Ebenezer Scrooge would deny funding the latest demanded government program. If wealth is so easy to create, many conclude only greed and cruelty are what stand between us and far greater prosperity for all.

But that is the very reason that fiat money is so subversive to the social order. In a sound money economy any new spending program can be funded only by an increase in taxes, an increase in debt, or by cutting existing funding. There is a real cost to each of these options. There is a real cost to printing money, too, but the cost is hidden. One does not see malinvestment at the time of money printing. Price increases are delayed and uneven, due to the Cantillon Effect whereby the early receivers of new money are able to purchase goods and services at existing prices. Later receivers or those who do not receive the new money at all suffer higher prices and a reduction in their standard of living. Even then most people do not link higher retail prices with a previous expansion of the money supply.

It would be hard to invent a more effective method for the destruction of modern society. As Pogo would say, “We have met the enemy and he is us.”

…let’s say a $1 billion to a country like Indonesia or Ecuador — and this country would then have to give ninety percent of that loan back to a U.S. company, or U.S. companies, to build the infrastructure — a Halliburton or a Bechtel. These were big ones. Those companies would then go in and build an electrical system or ports or highways, and these would basically serve just a few of the very wealthiest families in those countries. The poor people in those countries would be stuck…

The definition of foreign aid and a NATO membership requirement.

The Bretton Woods Committee, a globalist organization in the crony worst sense, is out with a propaganda video celebrating the 75th anniversary of the 1944 conference at Bretton Woods, which has launched decades of crony international economic management.

The video skips over the collapse of the Bretton Woods exchange rate system.

And it doesn’t explain that the greater Bretton Woods system was a crony system built on US dollars that resulted in massive dollar printing beyond foundational gold supplies.

In the Bretton Woods system, the United States pyramided dollars (in paper money and in bank deposits) on top of gold, in which dollars could be redeemed by foreign governments; while all other governments held dollars as their basic reserve and pyramided their currency on top of dollars.

Under this system, the US never stopped printing dollars. Rothbard again:

Europe did have the legal option of redeeming dollars in gold at $35 an ounce. And as the dollar became increasingly overvalued in terms of hard money currencies and gold, European governments began more and more to exercise that option. The gold-standard check was coming into use; hence gold flowed steadily out of the United States for two decades after the early 1950s, until the US gold stock dwindled over this period from over $20 billion to $9 billion. As dollars kept inflating upon a dwindling gold base, how could the United States keep redeeming foreign dollars in gold — the cornerstone of the Bretton Woods system?

And then the collapse came:

On August 15, 1971, at the same time that President Nixon imposed a price-wage freeze in a vain attempt to check bounding inflation, Mr. Nixon also brought the postwar Bretton Woods system to a crashing end. As European central banks at last threatened to redeem much of their swollen stock of dollars for gold, President Nixon went totally off gold. For the first time in American history, the dollar was totally fiat, totally without backing in gold.

And, of course, as John Perkins explained in Confessions of an Economic Hit Man, the Bretton Woods conference also formed the World Bank and the IMF. They are the muscle that provide loans (or back up loans) to nations that will never be able to pay them back on planned terms. Then the IMF and World Bank step in again to muscle the countries to pay back the loans via a resource grab or on the backs of local taxpayers. (For a recent example, think the Greek financial crisis.)

[M]y real job was deal-making. It was giving loans to other countries, huge loans, much bigger than they could possibly repay. One of the conditions of the loan — let’s say a $1 billion to a country like Indonesia or Ecuador — and this country would then have to give ninety percent of that loan back to a U.S. company, or U.S. companies, to build the infrastructure — a Halliburton or a Bechtel. These were big ones. Those companies would then go in and build an electrical system or ports or highways, and these would basically serve just a few of the very wealthiest families in those countries. The poor people in those countries would be stuck ultimately with this amazing debt that they couldn’t possibly repay. A country today like Ecuador owes over fifty percent of its national budget just to pay down its debt. And it really can’t do it. So, we literally have them over a barrel. So, when we want more oil, we go to Ecuador and say, “Look, you’re not able to repay your debts, therefore give our oil companies your Amazon rain forest, which are filled with oil.”…

We called ourselves e.h.m.’s. [economic hit men]. It was tongue-in-cheek. It was like, nobody will believe us if we say this, you know?…

The World Bank provides most of the money that’s used by economic hit men, it and the I.M.F.

Of course, nothing about this in the propaganda video below. Everything dome at the Bretton Woods conference was according to this video just wonderful.