Of course, Krugman’s confident dismissal of those Biden-hating doomsayers blew up in his face, as CPI inflation kept ratcheting higher and higher. In a December 2021 NYT column, Krugman threw in the towel and admitted he had been wrong, but in his own special way (again, with my bolding):

The current bout of inflation came on suddenly…. Even once the inflation numbers shot up, many economists—myself included—argued that the surge was likely to prove transitory. But at the very least it’s now clear that “transitory” inflation will last longer than most of us on that team expected…

Everything is transitory. The only thing that never changes is change.

https://mises.org/wire/keynesians-and-market-monetarists-didnt-see-inflation-coming

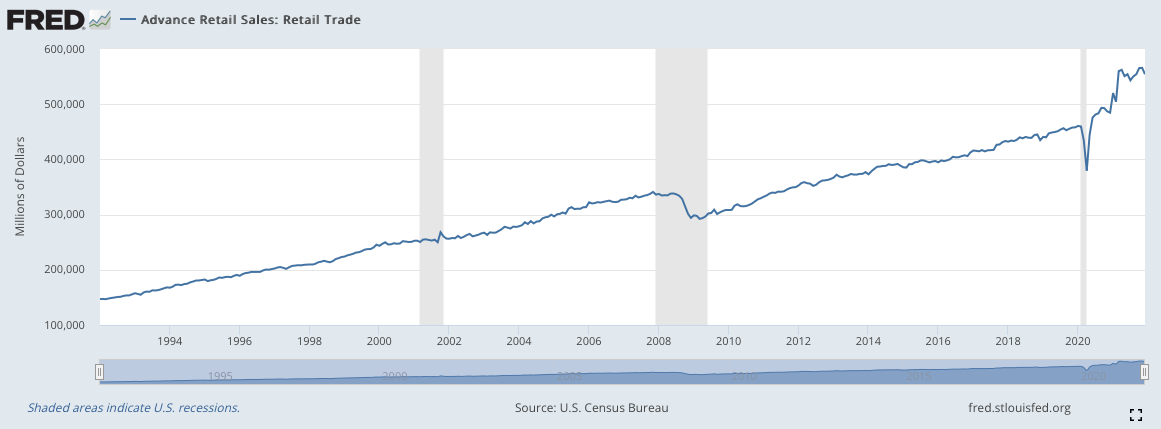

The government’s latest report puts the twelve-month official consumer price inflation rate at 8.5 percent, the highest since December 1981:

As economists debate the causes of, and cure for, this price inflation, it’s worth recounting which schools of thought saw it coming. Although individuals can be nuanced, generally speaking the Austrians have been warning that the Fed’s reckless policies threaten the dollar. In contrast, as I will document in this article, two of the leaders of the Keynesian and market monetarist schools didn’t see this coming at all.

My Worst Professional Mistake

Before diving into it, I need to address a problem: my hands-down worst professional mistake occurred during the early years of the Fed’s “QE” (quantitative easing) programs, when I made bets on (consumer price) inflation with two economist colleagues. I ended up losing those bets and thereby gave Paul Krugman the opportunity to lecture me on my intellectual dishonesty because I clung to my (ostensibly falsified) Austrian model even after my prediction blew up in my face. Indeed, if you check out my Wikipedia entry, you’ll see that apparently my life story is that I was born, got my PhD, and lost an inflation bet—in that order. (For those interested in the details, I summarize the episode with relevant links in this postmortem blog post. I also participated in a 2014 Reason symposium along with Peter Schiff and others, commenting on the lack of inflation.)

Ever since the rounds of QE failed to yield surging consumer price inflation at the scale some of us warned of, the Keynesians and market monetarists understandably ran victory laps, saying that they were to be trusted over those permabear Cassandra Austrians. (To be sure, the market monetarists were far more civil about it than the prominent Keynesians.) So it is not with gloating or vindictiveness that I write the present article, but rather I do it to set the record straight and document for posterity that the leading Keynesians and market monetarists totally missed this bout of price inflation.

The Keynesians Camp: Paul Krugman and Klaus Schwab

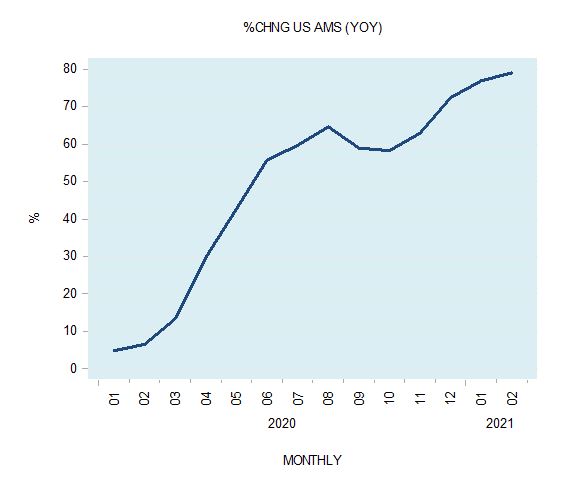

Let’s do the fun one first: Paul Krugman has not fared well in light of our current inflationary experience. As late as June 2021, Krugman wrote an article in the New York Times titled “The Week Inflation Panic Died.” Here are some key excerpts, with my bold added, and keep in mind that when Krugman wrote this, the most recent Consumer Price Index (CPI) inflation rate was only 4.9 percent:

Remember when everyone was panicking about inflation, warning ominously about 1970s-type stagflation? OK, many people are still saying such things, some because that’s what they always say, some because that’s what they say when there’s a Democratic president….

But for those paying closer attention to the flow of new information, inflation panic is, you know, so last week.

Seriously, both recent data and recent statements from the Federal Reserve have, well, deflated the case for a sustained outbreak of inflation … [T]o panic over inflation, you had to believe either that the Fed’s model of how inflation works is all wrong or that the Fed would lack the political courage to cool off the economy if it were to become dangerously overheated.

Both beliefs have now lost most of whatever credibility they may have had….

The Fed has been arguing that recent price rises are similarly transitory … The Fed’s view has been that this episode, like the inflation blip of 2010–11, will soon be over.

And it’s now looking as if the Fed was right …

Be seeing you