At its September 2024 meeting, the Fed’s FOMC cut the target federal funds rate by a historically large 50 basis points and then justified this cut on the grounds that “The Committee has gained greater confidence that inflation is moving sustainably toward 2 percent, and judges that the risks to achieving its employment and inflation goals are roughly in balance.”

The FOMC again cut the target rate in November and then again in December. Each time, the FOMC’s official statement said something to the effect of “[price] inflation is headed to two percent. Specifically, the November statement said “[Price inflation] has made progress toward the Committee’s 2 percent objective.” The December statement said exactly the same thing.

It remains unclear what motivated the FOMC to slice the target rate so drastically in September. Was it a cynical political ploy to stimulate the economy right before an election? Or was the Fed spooked by weak economic data? We don’t know, and the Fed is a secretive organization.

But whatever the Fed actually believes, the committee’s claims about “greater confidence” in falling price inflation is now gone. The FOMC announced in January that it would not lower the target rate, and the FOMC also removed from its official statement the line about making progress “toward the Committee’s 2 percent objective.” That sentence disappeared from the written statement, although Powell, in the press conference, apparently felt the need to remind the audience that “Inflation has moved much closer to our 2 percent longer-run goal…” He nonetheless failed to mention anything about continued progress.

It looks increasingly like all that confidence about “sustainable progress” on price inflation back in September—in the heat of election season, of course—was just one of the Fed’s many bogus, politically motivated forecasts.

Even if the Fed truly is motivated by the official data, though, it’s clear that the Fed now has good reason to downplay talk of declaring victory on the Fed’s two-percent inflation goal.

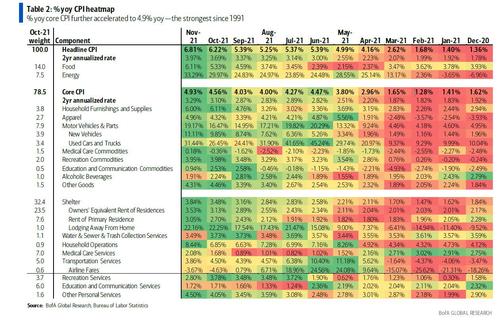

Recent official data—which generally reflects the best scenario that government bean counters can muster—shows plenty of bad news in this area. According to the Fed’s preferred inflation measure—PCE inflation—year-over-year price inflation reached an eight-month high in December, at 2.6 percent. (December is the most recent available number on PCE.) If we look at January’s headline CPI inflation, released on Wednesday, the picture is even worse. Year-over-year CPI inflation hit a nine-month high in January, at 3.0 percent, and month-to-month growth was at an eighteen-month high of 0.5 percent.

Thanks to the Fed’s unrestrained embrace of monetary inflation from 2020 to 2022, American consumers are still facing the grim reality of rising prices on basic necessities. In January’s CPI report, some of the largest jumps in prices were in food (2.5 percent), energy services (2.5 percent), other services (4.3 percent) and shelter (4.4 percent).

Wholesale prices also suggested that we won’t be seeing much relief from price inflation. According to new producer price index numbers, released on Thursday, year-over-year growth in the PPI reached a 24-month high of 3.5 percent. This is bad news for those hoping that the Fed’s predictions of falling prices might somehow come true. CNN delivered the bad news on Thursday: “The stronger numbers seen in Thursday’s PPI will tend to translate into continued consumer price inflation through the middle of the year.”

So why do these “experts” blame large corporations for something—price inflation—they do not cause? Because the objective is to increase government control of the economy and destroy private business that are large enough to be economically independent. They do not care about small businesses because those are already asphyxiated by taxes and small and medium enterprises are easily forced to depend on the government.

The current “dual” between the two mandates is to reduce price inflation by increasing interest rates to increase unemployment and kill businesses to choke off aggregate demand.

The Federal Reserve has a legal dual mandate to minimize unemployment and price inflation. The current “dual” between the two mandates is to reduce price inflation by increasing interest rates to increase unemployment and kill businesses to choke off aggregate demand. This has been the most important economic and investment issue this year and this dual minimization procedure has dominated Fed policy for at least three-quarters of a century.

This is odd given that the Fed is in the business of creating money, the cause of price inflation, and it is responsible for all the largest surges in unemployment since its founding in 1913. Employing an army of monetary economists, macro theorists, and statisticians, the Fed appears to be pursuing its quixotic quest of the Phillips curve sweet spot of minimizing inflation and unemployment.

The real mandate of the Fed is serving its masters, the political elites, by financing government spending and debt, bailing out cronies, and supporting the political process, including the Fed’s own interests. Everything else, including the inflation and unemployment rates are derivative of the primary mandate. The so-called dual mandate is just subterfuge to protect the Fed’s “confidence game.”

The Quest of the False Mandate

In The Fed Explained: What the Central Bank Does, we learn how control of the Fed is “decentralized.” This might sound good to some supporters of the free market. However, any hint of decentralization, such as the importance of District Banks, is long gone and the remnant is merely a diversion or historical curiosity. Of the twelve votes on the Federal Open Market Committee (FOMC) there are only four of twelve rotating District Bank presidents voting, plus the President of the New York Fed. The central Board of Governors in Washington DC has seven voting members who are appointed by the President and confirmed by the Senate and has nearly twice the voting power over interest rate decisions. Plus, the Chairman (Powell) has the power of the bully pulpit and is the consensus builder on the FOMC.

We are also told of the balancing of public and private (banks’) interests controlling the Fed and some free-market supporters latch onto the influence of the private sector as an effective check on the Fed’s enormous economic power. Big banks do work directly with the Fed in “open market operations” and interact in the day-to-day business of banking regulation. Commercial banks have some voting power within the District Banks. However, this influence is contingent on political goals and even the big banks can be pawns in the Fed’s political chess game. Their shares are “nonnegotiable” and are nothing like shares in private corporations. Banking interests are clearly derivative, and the Fed has thrown such interests overboard when necessary, such as with the Savings and Loan Crisis or Lehman Bros. In any case, the union of public and private interests is the ultimate source of corruption and can be the greatest threat to human liberty. Such private interests are clearly not a bulwark of liberty.

It is true that the Federal Reserve Act of 1913 was established and intended to be a cartel device for the banks and some banks are better protected than others. Marx and Engels (1848) called for the establishment of central banks and thereafter Americans were increasingly duped by socialist ideology. This socialist influence was an important force during the so-called Progressive Era (1890–1920). History textbooks make the Federal Reserve Act appear to be the result of a coalition of popular interests. However, the big banks and their academic technocrats controlled by political elites, created and controlled the legislative campaign with their “independent” National Monetary Commission.

A final and critical canard about the Fed is its “independence.” We are told that the Fed must be independent of political power to carry out its mandates and be effective. In this vein, if the Fed were to succumb to political pressures, then it would continually increase the money supply and suppress interest rates below market determined levels, especially before elections. This they tell us would destabilize the economy and might lead to hyperinflation the way it does under dictatorships where central banks do not have independence. I’m sure the Fed would love to be independent, but they are controlled by powerful office holders who are in turn controlled by the elites. As Ryan McMaken reminds us, “Fed independence is a fairy tale academic economists like to tell their students” and they are biased toward the inflationary mandate.

This is because the Fed’s strategy for reducing the historic price inflation now plaguing the economy — caused by the Fed’s unprecedented low or zero interest rate policies — is to increase unemployment in order to decrease consumer spending. In his speech to the annual monetary policy conference in Jackson Hole, Wyoming, Fed Chair Jerome Powell reiterated his commitment to increasing unemployment, or, as he puts it, “softening the labor markets.”

The Federal Reserve was no doubt troubled by July’s decline in the US unemployment rate to 4.5 percent and increase in job openings to 11.2 million. This is because the Fed’s strategy for reducing the historic price inflation now plaguing the economy — caused by the Fed’s unprecedented low or zero interest rate policies — is to increase unemployment in order to decrease consumer spending. In his speech to the annual monetary policy conference in Jackson Hole, Wyoming, Fed Chair Jerome Powell reiterated his commitment to increasing unemployment, or, as he puts it, “softening the labor markets.”

Powell is correct that reducing price inflation is urgent. He is also correct that doing so will increase unemployment and slow economic growth. The Fed’s efforts to bring down inflation by increasing interest rates will also make it harder for average Americans to obtain home mortgages, purchase a car, or even pay their utility bills. Those hardest hit by the Fed’s “softening of labor markets” are also the primary victims of the Fed-created price inflation. This demonstrates the insanity and cruelty of the fiat money system, which enriches the elites while improvising the masses.

Well-connected members of the financial elite and crony capitalists benefit from the Federal Reserve’s money creation, as they are the first recipients of the new money. This enables them to increase their purchasing power before the new money has caused general price inflation. By the time the money creation has impacted the middle and working classes, the economy is racked with widespread price inflation. Therefore, a nominal gain in wages is not enough to compensate for the real price increase. So average Americans suffer from both Fed-created inflation and the Fed’s attempts to rein in that inflation.

It is amazing that more individuals do not question the idea that inflation, recessions, unemployment, and booms and busts are necessary features of a sound monetary system. Even many otherwise staunch defenders of free markets maintain a child-like faith in central banking. Some conservatives support “reforming” the Fed by making it follow a “rules-based” monetary policy. These conservatives do not understand that the problem is the existence of a central bank with the power to manipulate the currency.

Many progressives recognize the damage the Fed does to average Americans when it increases interest rates. However, their “solution” is a cure worse than the disease: make the Fed maintain low interest rates (and thus high inflation) in perpetuity—or until the continued devaluation of the currency via inflation causes a dollar crisis, leading to a major economic calamity. The main victims of this crisis will, of course, be the very Americans progressives claim to care about.

The Federal Reserve’s failure to fulfill its dual mandate of producing stable prices and full employment, combined with the damage it inflicts on the American people, make the best case for changing our monetary policy. A stable currency, safe from manipulation by politicians or central bankers, would provide the basis for long term prosperity that benefits everyone, not just the crony capitalists and the power-hungry politicians. The first steps in this transition are to finally pass audit the Fed legislation and continue the efforts to pass state laws recognizing precious metals as legal tender.

In early 2020, the economic was weakening after more than a decade of remarkably slow economic growth and rising reliance on monetary expansion to prevent the implosion of Fed-created economic bubbles. But then covid happened, and the Fed blamed the disease for the economic collapse and inflation that followed. Now the war will provide yet another way for the Fed and its economists to claim they were doing a great job, and it would have all been a great success if not for the Russians.

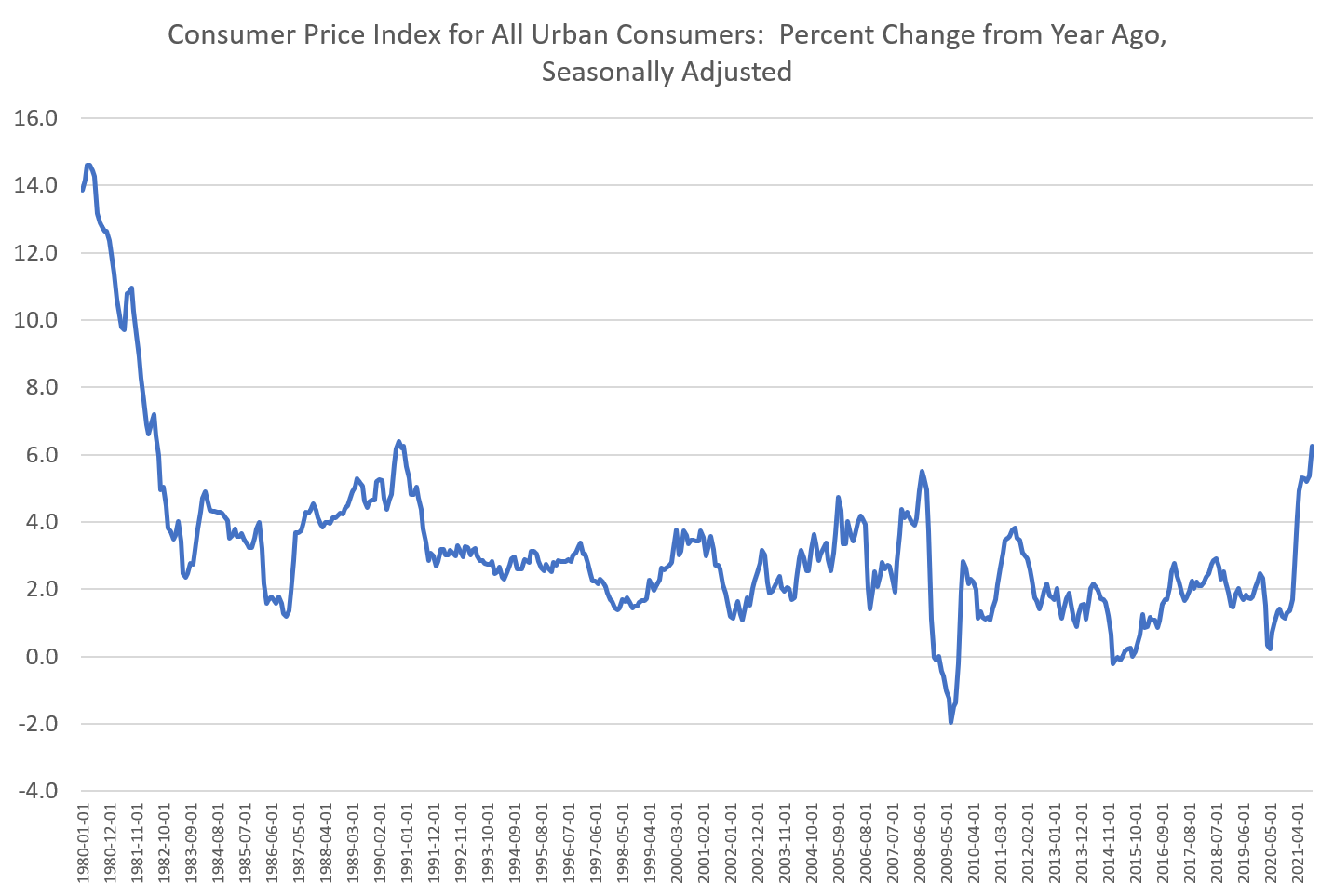

According to new data released by the Bureau of Labor Statistics, price inflation in February rose to the highest level recorded in more than forty years. According to the Consumer Price Index for February, year-over-year price inflation rose to 7.9 percent. It hasn’t been that high since January 1982, when the growth rate was at 8.3 percent.

February’s increase was up from January’s year-over-year increase of 7.5 percent. And it was well up from February 2021’s year-over-year increase of 1.7 percent.

A clear inflationary trend began in April 2021 when CPI growth hit the highest rate since 2008. Since then, CPI inflation has accelerated with year-over-year growth nearly doubling over the past 11 months from 4.2 percent to 7.9 percent.

For most of 2021, however, Federal reserve economists and their PhD-wielding allies in academia and the media insisted it was “transitory” and would soon dissipate. By late 2021, however, economists began to admit they were “surprised” and had no explanation for the inflation. (What one actually learns while obtaining a PhD in economics apparently has nothing to do with understanding money or prices.) Jerome Powell then declared that the Fed would prevent inflation from becoming “entrenched.”

Now, high level economists have changed their tune again with Janet Yellen admitting this week that “We’re likely to see another year in which 12-month inflation numbers remain very uncomfortably high.” Yellen had earlier predicted that CPI inflation would drop to around 3 percent, year over year, by the end of 2022.

Yellen was also careful to attempt political damage control by insinuating that price inflation is a result of uncertainty over the Russia-Ukraine war.

Never mind, of course, that the inflation surge began last year and that January’s CPI inflation rate was already near a 40-year high. The current crop of embargoes and bans on Russian oil imports implemented during March were not drivers of February’s continued inflation surge.

Few members of the public, however, will bother with these details, and this will benefit both the Fed and the administration. As far as the Fed is concerned, the important thing is to never, ever admit that price inflation is really being driven by more than a decade of galloping Fed-fueled monetary expansion (aka money printing). This was done largely at the behest of the White House and Congress to keep interest on the debt low and government spending high.

So, we can expect the administration to portray inflation as “Putin’s fault.” In a Friday speech to Democratic activists, Biden even claimed the high inflation rates are not due to “anything we did.” The tactic will no doubt work to convince many. But it’s unclear how many.

After the Consumer Price Index surged last year to its highest level since 1982, politicians are feeling pressure from constituents to do something about it.

Last Monday, President Joe Biden announced $1 billion in grants, loans, and other assistance for small meat producers. Another costly government program will, supposedly, help tame rapidly rising beef and poultry costs.

Four giant companies control 85% of the market for meat—raking in massive profits while families pay higher prices. I’m glad @POTUS is taking steps to create a more competitive beef and poultry industry. We need to break up Big Ag and lower prices. https://t.co/EHQZWaD2du

Massachusetts Senator Elizabeth Warren has been on a tear lately, and there is a startling commonality between all these ideas:

Prices at the pump have gone up. Why? Because giant oil companies like @Chevron and @ExxonMobil enjoy doubling their profits. This isn’t about inflation. This is about price gouging for these guys & we need to call them out. pic.twitter.com/kxiQkC2tYa

Consolidation in the semiconductor industry is causing shortages and supply chain bottlenecks that increase consumer prices and hurt workers. I’m urging @SecRaimondo to act swiftly to increase competition. https://t.co/Y7Izd6X0Fl

This is your brain on fiat monetary systems and central banking: price inflation is caused by everything except for printing loads of new money.

If Senator Warren believes that prices increase because of the greed of price gouging companies, does she believe that when prices fall, it is the result of corporate benevolence?

In any case, what we though this summer was just a joke appears to be coming true, because as the BLS has reported, starting next month it will adjust the weights for its Consumer Price Index basket, which will be calculated “based on consumer expenditure data from 2019-2020.” Alas, there is no further detail on this critical topic, although we will take any bet that post-revision reported inflation will drop because, well, “adjustments.”

Earlier this year, when inflation was still “transitory” two Fed chairs, Powell and Bernanke, made comments which we joked only make sense if the definition of inflation is changed:

*POWELL:FOMC PREPARED TO ADJUST POLICY IF EXPECTATIONS GO BEYOND

by changing definition of PCE and CPI — zerohedge (@zerohedge) July 28, 2021

BERNANKE: COMMODITY PRICES WON’T ADD TO INFLATION GOING FORWARD

Why? Are we changing the definition of CPI again — zerohedge (@zerohedge) August 25, 2021

Sadly, our feeble attempts at humor were not unjustified, and as any economic history buff knows the US dramatically changed how it calculates consumer inflation back in the 1980s, an event extensively covered by AllianceBernstein former chief economist Joseph Carson on this website in the past (see “Consumer Price Inflation: Facts vs. Fiction“) with the most important difference being that while the CPI of the 1970s included house price inflation, the current measure does not. Instead, home price pressures have been swept in the purposefully nebulous Owner-Equivalent Rent which can be whatever politicians wants it to be (there have been other definitional changes, see here, here, here and here for more). Bottom line, however, is that if today’s CPI did include house prices in its measurement, the currently reported inflation numbers for house price inflation would push CPI (and core CPI) to double-digit gains.

Of course, it is politically inconvenient to report true inflation is – just see what happens in any banana republic where society is fed up with runaway inflation. It’s also why politicians on both sides of the aisle are always eager to tweak the definition of inflation ever so slightly (or not so slightly) so it appears to be less than it truly is. After all, for them masking reality is a matter of political survival.

In any case, what we though this summer was just a joke appears to be coming true, because as the BLS has reported, starting next month it will adjust the weights for its Consumer Price Index basket, which will be calculated “based on consumer expenditure data from 2019-2020.” Alas, there is no further detail on this critical topic, although we will take any bet that post-revision reported inflation will drop because, well, “adjustments.”

In the same press release, we also read that “the BLS considered interventions, but decided to maintain normal procedures”… whatever those are. Said otherwise, the BLS may not be “intervening” for now, but when the inflationary rubber hits the road next year with the midterms coming up fast and Dems ratings still in the dumps, we doubt that the BLS will have any qualms to “intervene.”

Incidentally, this “update” may explain the conviction behind Biden’s statement today: in a statement after the blistering hot CPI report came out…

… Joe Biden said that despite experiencing the most rapid inflation in almost 40 years in November, U.S. price increases are slowing, in particular for gasoline and cars.

“Today’s numbers reflect the pressures that economies around the world are facing as we emerge from a global pandemic — prices are rising… But developments in the weeks after these data were collected last month show that price and cost increase are slowing, although not as quickly as we’d like,” he said. Biden’s chief of staff Ronald Klain chimed in too:

We’ve made progress, but we’ve got to get prices down, and people have to feel the progress at their kitchen tables.https://t.co/YH102YVlQp — Ronald Klain (@WHCOS) December 10, 2021

Well, all that prices needs to slow “as quickly as we’d like” at least in government reports such as the CPI, is for the BLS to give them a gentle nudge lower.

Nonetheless, it is entirely possible that inflation rates could quickly turn downward again in coming months. That could occur if recession sets in with businesses and households unable to pay off their debts. If that happens, monetary deflation will set in and demand will decline, leading to a real drop in price inflation. Of course, that won’t exactly do wonders for real wages, either.

The Bureau of Labor Statistics reported Wednesday morning that prices rose 6.2% on a year-over-year basis in October. That’s the highest YOY rate since December 1990 when the CPI was also up 6.2 percent.

October’s rate was up from 5.3 percent in September, and remains part of a surge in the index since February 2021 when year-over-year growth was still muted at 1.6 percent.

Not surprisingly, producer prices surged in October as well. The producer price index for commodities in October was up 22.2 percent, year over year, reaching a 48-year high. We must go back to November 1974 to find a higher PPI increase—at 23.4 percent.

Asset price inflation has naturally continued unabated at well, with the result being rising housing costs. In addition to the CPI’s 31-year high, home prices in the second quarter surged near to a 42-year high. According to the Federal Housing Finance Agency’s home price index, home price growth reached 11.9 percent in the second quarter of this year. Since 1979, only the second quarter of 2005—also with 11.9 percent growth—showed home-price growth as high.

None of this means policymakers will diagnose the problem properly, however. We should expect the discussion around inflation in Washington to keep missing the point and denying any connection to the central bank or to monetary inflation.

For example, rising prices are so obvious now that not even the administration can ignore them anymore. Today, the White House released a statement in which President Biden admitted: “… today’s report shows an increase over last month. Inflation hurts Americans pocketbooks”

Yet the administration continues to be very much in denial about the causes of price inflation. The Biden statement continues:

I have directed my National Economic Council to pursue means to try to further reduce these costs, and have asked the Federal Trade Commission to strike back at any market manipulation or price gouging in this sector.

As if “price gouging” were the cause of nationwide price inflation!

If it were “gouging,” we’d be seeing increases only in the areas where so-called gouging is taking place. Moreover, that would mean a decline in spending—and thus price deflation—in areas where the gouging isn’t taking place. The overall effect would be price stability.

Similarly, the administration has also tried to blame inflation on a lack of childcare. In an incoherent series of non sequiturs, Secretary of Transportation Peter Buttigieg this week claimed that paid family leave is “part of [the administration’s] tool kit to fight inflation.” Buttigieg simultaneously claimed that paid family leave means more people can take time off from work, and yet this somehow will also translate into more people going back to work. While it’s true more workers could help temper—to some extent—upward pressure on prices, more paid family leave would contribute nothing to this “solution” to price inflation. Rather, it’s apparent the memo went out at the administration that every policy must now be tied into some kind of plan to fight inflation—no matter how tenuous the connection.

Yet we should expect more of this sort of blind grasping at excuses for our economic malaise as time goes on. The same strategy was used by the Ford administration in the dark days of the mid1970s and the “Whip Inflation Now” campaign. The administration then claimed that the American public should fight inflation through strategies such as planting a vegetable garden at home.

Then, as now, the regime refused to admit that rising monetary inflation had anything to do with rising prices. Instead, we’re told it must be a lack of daycare services or “price gouging.”

A Second Strategy: Total Denial

But some in the administration are sticking to their narrative that there’s nothing at all to see here. Janet Yellen, for example, declared on Tuesday that “I’d expect price increases to level off, and we’ll go back to inflation that’s closer to the 2% that we consider normal.” She insists the Fed is very much in control of the situation and won’t allow 1970’s style inflation to occur.

What Yellen fails to mention is that even if inflation rates of, say, four to six percent, last only a year, middle class workers won’t make up these losses later just because inflation falls again at some point to “to the 2% that we consider normal.” After all, this year’s declines in real average weekly wages means real hardship for many people, even if Janet Yellen will be just fine with her private driver shuttling her from her luxury home to opulent cocktail parties all the while.

But not everyone is as uninterested in the effects of inflation as Janet Yellen. As MSNBC reports:

“For now, inflation is going to continue to run above very solid wage growth,” said Joseph LaVorgna, chief economist for the Americas at Natixis and former chief economist for the National Economic Council during the Trump administration. “This is why when you look at consumer confidence, it’s really taking a beating. Households do not like the inflation story, and rightly so.”

For at least one MSNBC columnist, though, people don’t know how good they have it. On Monday, James Surowiecki insisted everyone is better off and discussion of inflation amounts to little more than fear mongering. He writes:

Otherwise, as noted earlier, rising interest rates would collapse the debt pyramid and result in a collapse in output and employment. It is, therefore, no wonder that the Fed is doing whatever it can to hide the inflationary consequences of its policy from the public:

Speaking at the Jackson Hole meeting on August 27, 2021, Federal Reserve (Fed) chairman Jerome J. Powell indicated that he supported “tapering” toward the end of this year and hastened to add that interest rate hikes are still a long way off. The term “tapering” means that the central bank reduces its monthly purchases of bonds and slows down the monthly increase in the quantity of money accordingly. In other words, even with tapering, the Fed will still churn out newly printed US dollar balances, but to a lesser extent than before; that is, it will still cause monetary inflation, but less than before.

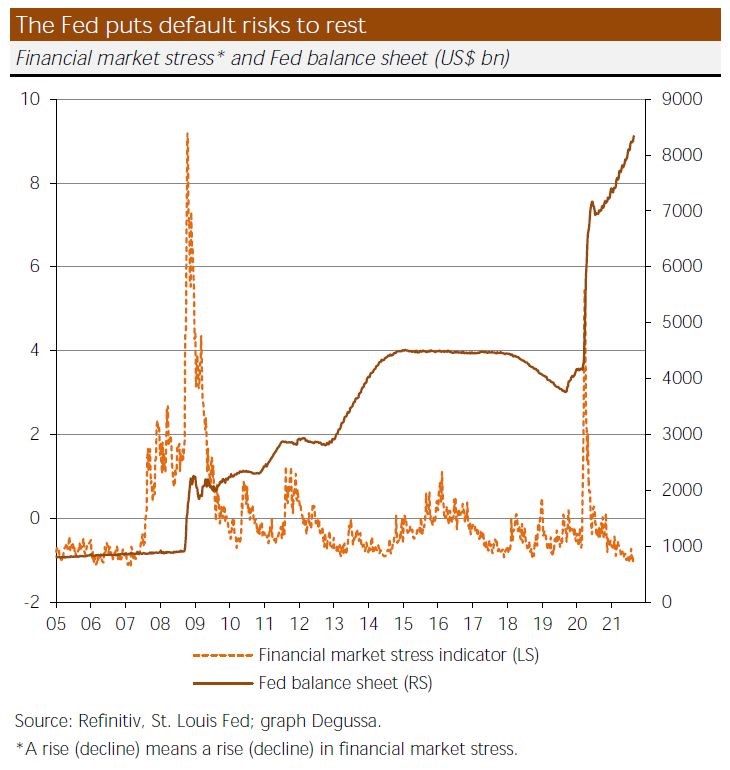

Financial markets were not alarmed by the Fed’s announcement that it might take its foot off the accelerator pedal a little: ten-year US Treasury yields are still trading at a relatively low level of 1.3 percent, the S&P 500 stock index hovers around record highs. Could it be that investors do not believe in the Fed’s suggestion that tapering will begin soon? Or is tapering of much lower importance for financial market asset prices and economic activity going forward than we think? Well, I believe the second question nails it. To understand this, we need to point out that the Fed has put a “safety net” under financial markets.

As a result of the politically dictated lockdown crisis in early 2020, investors feared a collapse of the economic and financial system. Credit markets, in particular, went wild. Borrowing costs skyrocketed as risk premiums rose drastically. Market liquidity dried up, putting great pressure on borrowers in need of funding. It wasn’t long before the Fed said it would underwrite the credit market, that it would open the monetary spigots and issue all the money needed to fund government agencies, banks, hedge funds, and businesses. The Fed’s announcement did what it was supposed to do: credit markets calmed down. Credit started flowing again; system failure was prevented.

In fact, the Fed’s creation of a safety net is nothing new. It is perhaps better known as the “Greenspan put.” During the 1987 stock market crash, then Fed chairman Alan Greenspan lowered interest rates drastically to help stock prices recover—and thus set a precedent that the Fed would come to rescue in financial crises. (The term “put” describes an option which gives its holder the right, but not the obligation, to sell the underlying asset at a predetermined price within a specified time frame. However, the term “safety net” might be more appropriate than “put” in this context, as investors don’t have to pay for the Fed’s support and fear an expiry date.)

The truth is that the US dollar fiat money system now depends more than ever on the Fed to provide commercial banks with sufficient base money. Given the excessively high level of debt in the system, the Fed must also do its best to keep market interest rates artificially low. To achieve this, the Fed can lower its short-term funding rate, which determines banks’ funding costs and thus bank loan interest rates (although the latter connection might be loose). Or it can buy bonds: by influencing bond prices, the central bank influences bond yields, and given its monopoly status, the Fed can print up the dollars it needs at any point in time.

Or the Fed can make it clear to investors that it is ready to fight any form of crisis, that it will bail out the system “no matter the cost,” so to speak. Suppose such a promise is considered credible from the financial market community’s point of view. In that case, interest rates and risk premiums will miraculously remain low without any bond purchases on the part of the Fed. And it is by no means an exaggeration to say that putting a safety net under the system has become perhaps the most powerful policy tool in the Fed’s bag of tricks. Largely hidden from the public eye, it allows the Fed to keep the fiat money system afloat.

The critical factor in all this is the interest rate. As the Austrian monetary business cycle theory explains, artificially lowering the interest rate sets a boom in motion, which turns to bust if the interest rate rises. And the longer the central bank succeeds in pushing down the interest rate, the longer it can sustain the boom. This explains why the Fed is so keen to dispel the notion of hiking interest rates any time soon. Tapering would not necessarily result in an immediate upward pressure on interest rates—if investors willingly buy the bonds the Fed is no longer willing to buy, and/or if the bond supply declines.

But is it likely that investors will remain on the buy side? On the one hand, they have a good reason to keep buying bonds: they can be sure that in times of crisis, they will have the opportunity to sell them to the Fed at an attractive price; and that any bond price decline will be short lived, as the Fed will correct it quickly. On the other hand, however, investors demand a positive real interest rate on their investment. Smart money will rush to the exit if nominal interest rates are persistently too low and expected inflation persistently too high. The ensuing sell-off in the bond market would force the Fed to intervene to prevent interest rates from rising.

Otherwise, as noted earlier, rising interest rates would collapse the debt pyramid and result in a collapse in output and employment. It is, therefore, no wonder that the Fed is doing whatever it can to hide the inflationary consequences of its policy from the public: the steep rise in consumer goods price inflation is being dismissed as only “temporary”; asset price inflation is said to be outside the policy mandate, and the impression is given that increases in stock, housing, and real estate prices do not represent inflation. Meanwhile, the increase in the money supply—which is the root cause of goods price inflation—is barely mentioned.

However, once people begin to lose confidence in the Fed’s willingness and ability to keep goods price inflation low, the “safety net trickery” reaches a crossroads. If the Fed then decides to keep interest rates artificially low, it will have to monetize growing amounts of debt and issue ever-larger amounts of money, which, in turn, will drive up goods price inflation and intensify the bond sell-off: a downward spiral begins, leading to a possibly severe devaluation of the currency. If the Fed prioritizes lowering inflation, it must raise interest rates and reign in money supply growth. This will most likely trigger a rather painful recession-depression, potentially the biggest of its kind in history.

Against this backdrop, it is difficult to see how we could escape the debasement of the US dollar and the recession. It is likely that high, perhaps very high, inflation will come first, followed by a deep slump. For inflation is typically seen as the lesser of two evils: rulers and the ruled would rather new money be issued to prevent a crisis over allowing businesses to fail and unemployment to surge dramatically—at least in an environment where people still consider inflation to be relatively low. There is a limit to the central bank’s machinations, though. It is reached when people start distrusting the central bank’s currency and dumping it because they expect goods price inflation to spin out of control.

But until this limit is reached, the central bank still has quite some leeway to continue its inflationary policy and increase the damage: debasing the purchasing power of money, increasing overconsumption and malinvestment, and making big government even bigger, effectively creating a socialist tyranny if not stopped at some point. So, better stop it. If we wish to do so, Ludwig von Mises (1881–1973) tells us how: “The belief that a sound monetary system can once again be attained without making substantial changes in economic policy is a serious error. What is needed first and foremost is to renounce all inflationist fallacies. This renunciation cannot last, however, if it is not firmly grounded on a full and complete divorce of ideology from all imperialist, militarist, protectionist, statist, and socialist ideas.”1

1. Ludwig von Mises, “Stabilization of the Monetary Unit–from the Viewpoint of Theory (1923),” in The Cause of the Economic Crisis. And Other Essays before and after the Great Depression, edited by Percy L. Greaves Jr. (Auburn, AL: Ludwig von Mises Institute, 2006), p. 44, appendix.

Slowly, but surely, the public began to realize: “We have been waiting for a return to the good old days and a fall of prices back to 1914. But prices have been steadily increasing. So it looks as if there will be no return to the good old days. Prices will not fall; in fact, they will probably keep going up.” As this psychology takes hold, the public’s thinking in Phase I changes into that of Phase II: “Prices will keep going up, instead of going down. Therefore, I know in my heart that prices will be higher next year.” The public’s deflationary expectations have been superseded by inflationary ones.

Recently here on Mises Wire, Sammy Cartagena wrote a brilliant article demonstrating that Two Percent Inflation Is a Lot Worse Than You Think. In it, he demonstrates that the manageable 2 percent inflation year over year we all have gotten used to is a whole lot less manageable than we tend to think. But in it, he also cited explaining that “over 23 percent of all dollars in existence were created in 2020 alone.” From that he explains that while future inflation is important, he is focused on past inflation for the sake of his article, which is where these two articles diverge because this will be questioning future inflation. Anyone paying attention has seen that there has obviously been inflation this past year whether through price increases or more subtle ways to sneak inflation into the economy. However, when we look at the massive spending bills and the aforementioned fact that over 23% of dollars have just recently been ushered into existence, it leaves many asking why has there not been proportionally drastic inflation?

The major piece that is holding back even more inflation than we’ve already seen is a public expectation of a return to normal. The economy is exceedingly complicated and there are countless causal factors effecting this so I cannot say this is the only reason, but we can turn to The Mystery of Banking where we see Murray Rothbard go as far as claiming that “Public expectation of future price levels” is far and away the most important determinant of the demand for money. Rothbard goes on to cite his intellectual predecessor – Ludwig von Mises – to explain just how strongly expectations played a role in the German hyperinflation in 1923:

The German hyperinflation had begun during World War I, when the Germans, like most of the warring nations, inflated their money supply to pay for the war effort and found themselves forced to go off the gold standard and to make their paper currency irredeemable. The money supply in warring countries would double or triple. But in what Mises saw to be Phase I of a typical inflation, prices did not rise nearly proportionately to the money supply. If M in a country triples, why would prices go up by much less? Because of the psychology of the average of the average German, who thought to himself as follows: “I know that prices are much higher now than they were in the good old days before 1914. But that’s because of wartime, and because all goods are scarce due to diversion of resources to the war effort. When the war is over, things will get back to normal, and prices will fall back to 1914 levels.” In other words, the German public originally had strong deflationary expectations. Much of the new money was therefore added to cash balances and the Germans’ demand for money rose. In short, while M increased a great deal, the demand for money also rose and thereby offset some of the inflationary impact on prices.

As Rothbard explains, prices not rising in proportion to a radical increase in the money supply is not only understandable, it is actually to be expected. Sure, this current situation is not a wartime economy, however, as far as Rothbard’s explanation of the psychology of the average person goes, it is not all too different from the expectations during the war. Today the psychology of the average American leads to him thinking to himself “I know that prices are much higher now than they were in the good old days before 2020. But that’s because of the pandemic, and because all goods are scarce due to the unemployment from people who had to stay home during this dangerous time. When the pandemic is over, things will get back to normal, and prices will fall back to 2019 levels.” The problem with this expectation is that it cannot last forever. As Rothbard explains

Slowly, but surely, the public began to realize: “We have been waiting for a return to the good old days and a fall of prices back to 1914. But prices have been steadily increasing. So it looks as if there will be no return to the good old days. Prices will not fall; in fact, they will probably keep going up.” As this psychology takes hold, the public’s thinking in Phase I changes into that of Phase II: “Prices will keep going up, instead of going down. Therefore, I know in my heart that prices will be higher next year.” The public’s deflationary expectations have been superseded by inflationary ones.

Rothbard explains that these new expectations will intensify the inflation rather than holding it back. Rothbard also claims that there is no way of knowing when these expectations will finally shift because so many cultural, technological, geographical, and other factors affect any given population. As a result, we unfortunately can’t say when modern Americans will realize that prices are not headed back to their pre-pandemic levels and start having intensifying expectations. But however long it does take, the last point that we have to remember from Rothbard is his claim that “When expectations tip decisively over from deflationary, or steady, to inflationary, the economy enters a danger zone. The crucial question is how the government and its monetary authorities are going to react to the new situation.” While it is too late to not have created all that new money supply, when the day does come that we enter that danger zone, it is not too late for us to react appropriately and avoid that final phase III of hyperinflation but rather allow for a healthy deflationary bust allowing the economy to recover as it so desperately needs. Author:

Connor Mortell graduated from Texas Christian University with a BBA in finance, minoring in Chinese language and culture. After graduation he worked as a legislative aide in the Florida House of Representatives for just shy of two years. Currently he is an MBA student at Florida State University. As well he will be attending Mises University in summer 2021.

by Tyler Durden

by Tyler Durden

{kind=link}

{kind=link}